Build your Startup Dream Team

Find Startup-Obsessed Co-Founders, Experts, Peers, and Talent

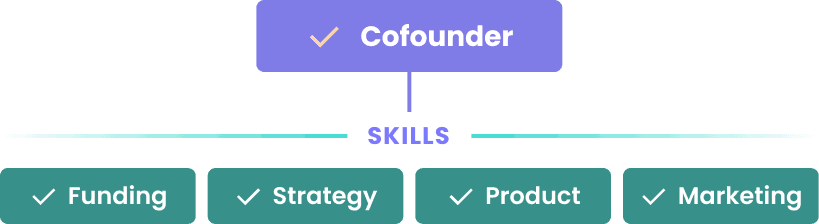

I am looking for:

Experience & Skills: select all that apply

Similar skills:

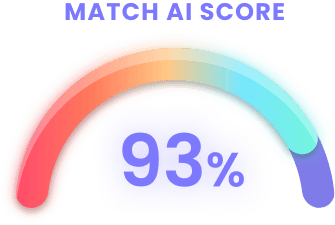

Good news! You have potential matches.

How it works

Step 1

Tell us what you need

Step 2

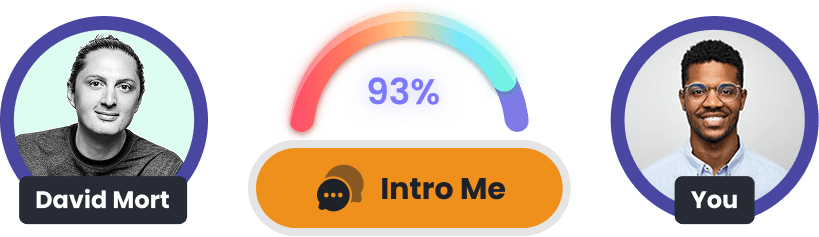

Our AI will match you instantly

Step 3

Grow Faster, Together

Featured Profiles

Andrew Crefeld

Co-Founder

Launched HouseLens in 2008 and was acquired in 2020. Starting a new company (on the side) called RentOrShare.IT.

Meg Schlabs

Graphic Design

Helping companies reach their audience through branding, graphics and web design since 2011.

Greg Welch

Advisor

Tech-focused Chief Executive with a proven track record of founding, building, and operating companies across multiple marketplaces.

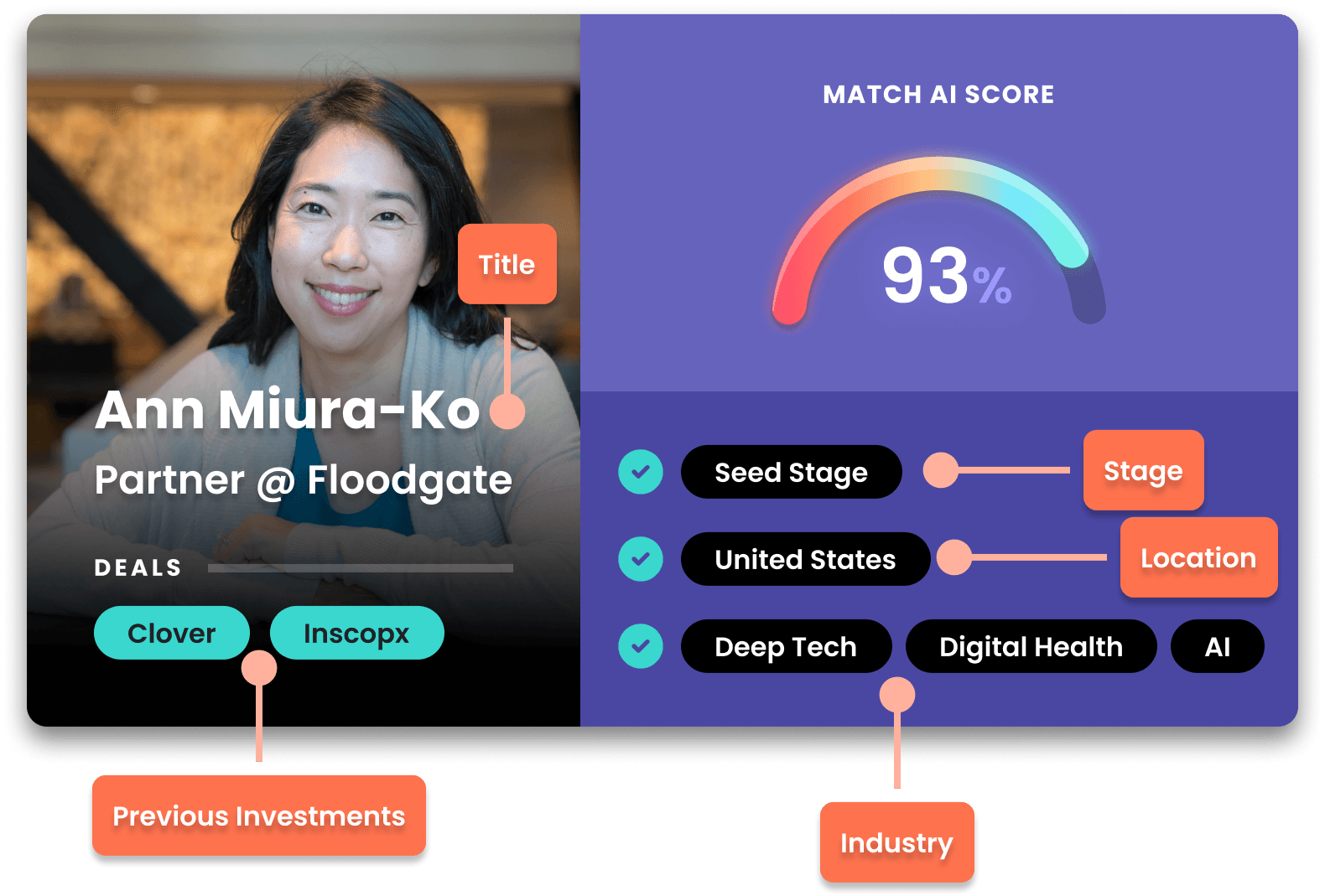

AI Precision Matching

Our AI instantly matches your exact startup needs with members perfectly scored to fit your requirements. We'll take hundreds of thousands of candidates and give you the absolute best fit to start with.

Co-Founders

Add the perfect compliment to your skill set with a Co-Founder who can offer technical, sales, marketing or fundraising skills. Give yourself tons of options to find the best possible long term fit.

Expert Advice

Tap into deep expertise in everything from Customer Acquisition to Technical Development to Legal issues from fellow Founders who have already figured out what you're wrestling with.

Founder Peers

Surround yourself with super-smart, like-minded Founders who really "get it" and can help you grow your business. Expand your business network while also building some cool new friendships along the way.

Startup Talent

Find the people you need to grow, from Developers to Designers to Marketing Managers, who are used to being paid with startup-style compensation and working on world-changing ideas.

Looking to join a world-changing startup?

Join here and start matching in less than a minute.